Why RBI Overseas Remittance Rules Are Changing

The Reserve Bank of India (RBI) is in the process of tightening the rules under the Liberalised Remittance Scheme (LRS), which enables resident Indians to remit money overseas for various personal reasons. This action is being taken to check abuse of the scheme and avoid the unauthorized or passive parking of funds in offshore banks.

While the LRS was introduced to facilitate global financial engagement for Indian residents, growing concerns over misuse have led the central bank to reevaluate its current approach. This article will examine the proposed changes in detail, analyze the rationale behind them, and assess their implications for individuals, financial institutions, and India’s broader macroeconomic landscape.

The Liberalised Remittance Scheme (LRS)?

A Quick Refresher

The Liberalised Remittance Scheme (LRS) is a scheme that permits resident individuals, even minors, to remit up to USD 250,000 per financial year for specific allowable transactions freely. They include:

- Foreign education

- Medical treatment overseas

- Travel and tourism

- Gifting to relatives overseas

- Investment in foreign equities, bonds, and property

But the scheme does not permit remittances for certain purposes, such as margin trading, purchasing lottery tickets, and certain leveraged instruments.

Why is the RBI Considering Restrictive LRS Rules?

- Foreign Currency Deposits Remittances

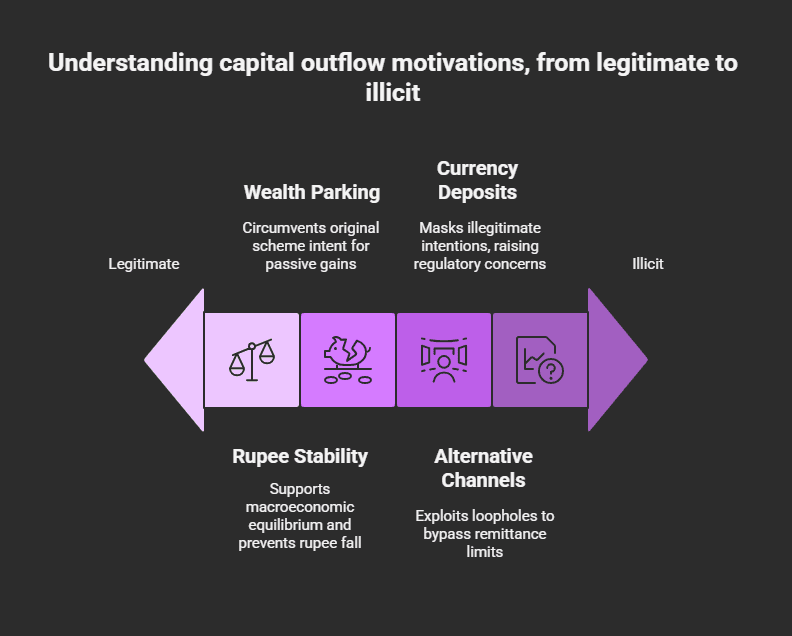

There has been a sudden remittance spike in foreign currency deposits, from $51.6 million in February 2025 to more than $173.2 million in March 2025. This increase is causing the RBI to raise an eyebrow, as it suspects some of it may not be for genuine reasons. - Passive Wealth Parking Concerns

RBI officials opine that some people are using LRS to passively park money overseas, opening fixed deposits or locked-in savings accounts in foreign banks, practices not originally meant under the scheme. - Rupee Stability and Forex Pressure

Unrestricted foreign remittances can erode India’s capital control regime and place a strain on foreign exchange reserves. In the wake of economic instability globally, India is taking a conservative approach towards outward capital flows that could result in rupee fall or macroeconomic disequilibrium. - Abuse Through Alternative Channels

There’s also a fear that residents are employing third-party remitters or family members overseas to avoid LRS ceilings, effectively doubling or tripling remittance capacity and diluting oversight.

Proposed Changes Under RBI’s New Remittance Rules

Ban on Foreign Fixed Deposits

RBI is likely to prohibit LRS funds from being used to open fixed deposits or similar interest-bearing accounts in overseas banks. This step is meant to block passive wealth storage that doesn’t serve any productive or investment purpose.

Impact:

Indians who are employing LRS as a legitimate channel to earn interest overseas will have to look for substitute, compliant financial instruments.

Blocking Locked-In Accounts

RBI also intends to prohibit remittances into “locked-in” accounts, which keep money locked up for a length of time and don’t allow repatriation. Such accounts could otherwise be used as quasi-tax shelters or offshore savings plans.

Tighter Reporting and Source Checks

Banks and authorized dealers are likely to be directed to strictly check the purpose as well as the source of remitted money, with further documentation needed for investments, gifts, and foreign family account remittances.

Aforementioned Changes Include:

- KYC/AML verification for every LRS application

- Documentary evidence of income source for high-value remittances

- Cross-verification of PAN and Aadhaar to check circular remittances

Curbing Third-Party Routing

The RBI can collaborate with the Income Tax Department and the Enforcement Directorate to determine the people remitting money through intermediaries or under other names. More data sharing between agencies is on the cards.

What’s Not Changing: Genuine Remittances Will Be Preserved

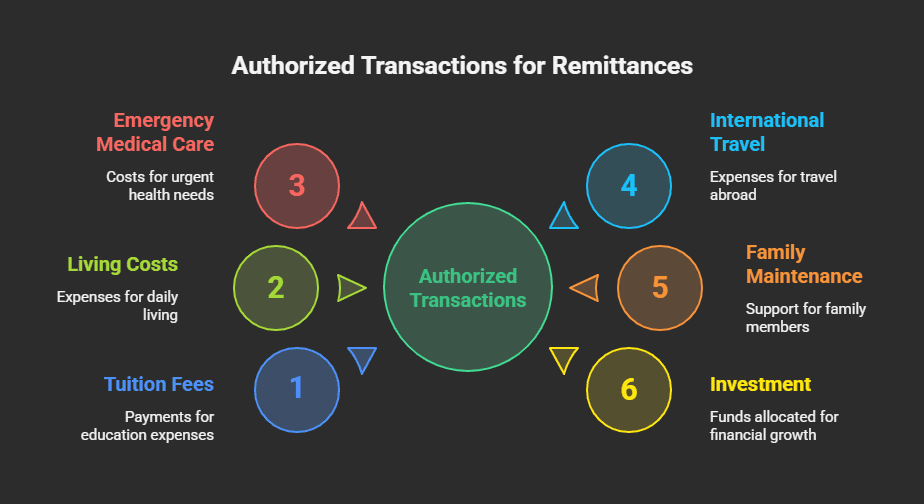

It’s worth mentioning that the new RBI overseas remittance guidelines won’t touch genuine transactions. The following are some purposes that continue to be completely permitted under LRS:

Authorized Transactions:

- Tuition fees and living costs of foreign students

- Emergency medical care

- International travel

- Maintenance of family members

- Investment in equity, debt, and mutual funds

The adjustments are not targeting these users but are meant to intercept abuse in the guise of legitimate remittances.

The Numbers Behind the Reform

A Look at Recent Trends

| Remittance Category | March 2024 ($ mn) | March 2025 ($ mn) |

|---|---|---|

| Foreign Deposits | 68.4 | 173.2 |

| Overseas Travel | 1,170.0 | 1,256.0 |

| Education | 370.2 | 348.6 |

| Investment in Equity/Mutuals | 92.4 | 103.0 |

| Gifting | 260.0 | 278.4 |

The precipitous increase in foreign deposits is the focus, while other categories are steady or modestly expanding.

International Comparisons: How Other Nations Manage Remittances

Both China and South Korea also have strongly controlled outward remittance systems. In China, for example, one can remit a mere $50,000 per year, and the purpose must be well substantiated. India’s Liberalized Remittance Scheme is fairly free by international standards, but with this freedom comes the risk of capital flight that the RBI wishes to counteract without punishing legitimate remitters.

Capital Account Convertibility: Not There Yet

India has been rather cautious in the past when it comes to capital account convertibility, i.e., free mobility of capital across borders. The RBI has shown an interest in evolving towards this, but only through the stringency of macroeconomic stability. Relaxing LRS norms too much would be at odds with this calibrated approach. Instead, the RBI is preferring calibrated controls in order to avoid systemic risks.

Financial Institutions Impact

Banks and Authorized Dealers (ADs)

- Will need to update internal risk-monitoring systems

- Must conduct stricter due diligence

- May see reduced commission revenues on deposit-related remittances

Fintechs and Investment Platforms

- Overseas investment apps might be subject to fresh documentation requirements

- May need to modify onboarding flows for Indian users

- Will have to distinctly flag such banned instruments as foreign FDs

Tax Consequences of the New Rules

TCS Under LRS Remains

Don’t forget: under the Finance Act 2023, a 20% Tax Collected at Source (TCS) is levied on foreign remittances over ₹7 lakh, unless for medical or educational reasons.

With the New Rules:

- Remittance can be rejected by RBI (e.g., for FDs), but will be rejected at bank level

- In such instances, the TCS withheld might have to be refunded or recovered later through ITR filing

What Do You Do As an LRS User?

If You’re a Student or a Tourist:

You’re not likely to be affected. Keep on sending money with due documentation and purpose codes.

If You’re an Overseas Investor:

Keep yourself informed about RBI notifications. Refrain from utilizing LRS to open any fixed-income deposit instruments overseas.

If You’re Sending High-Value Gifts:

Ensure the recipient’s details, relationship, and transfer reason are properly disclosed.

Always:

- Be income-tax compliant

- Do not use agents or intermediaries for remittances

- Adhere to RBI-allowed purposes only

When Will the New RBI Overseas Remittance Rules Be Announced?

As of mid-June 2025, the proposals stand in the consultation stage. The RBI is consulting the Finance Ministry and the authorized dealers (banks). The final guidelines will be notified shortly, perhaps before the close of Q2 FY 2025-26.

Final Thoughts: A Calibrated Tightening, Not a Clampdown

The new RBI foreign remittance regulations should not be seen as punitive or restrictive of personal liberty. Rather, they are a realistic tightening of loopholes facilitating passive wealth migration. The action aims to safeguard the economic interests of India without thwarting global mobility and legitimate financial ambitions.

If you’re using the LRS for real needs, education, travel, or family, you have little to worry about. But if you’re exploiting it as a route to move money offshore, the window may soon close.